Volatility is back! (Sort of)

“The time has come for policy to adjust” – Jerome Powell, 8/23, Jackson Hole

And with that short, concise admission the market finally acknowledged the rumor that had been circulating for months. Yes, the Fed is going to start cutting rates. Mind you, markets were expecting 6-7 cuts in December of 2023, and began pricing equities accordingly. That obviously didn’t happen, but now it is. The only question is how deep and at what speed. We will begin to get some answers on September 18th, the next FOMC meeting, and the overwhelming likelihood is a 25bps cut. Which, by all accounts the markets have already priced in.

The Fed Fund Futures are pricing 100 bps of cuts in 2024 With 25bps in September and 75bps between the November and December meetings, which implies one of those meetings will be a 50bps cut.

Inflation has been neutered. Hopefully. The American consumer may not be as sanguine on inflation as the Fed is. A trip to the grocery store, pharmacy, or a chat with any sort of insurance agent reminds consumers that higher prices are still prevalent.

Anyways, the Fed is now solely centering their attention on the labor markets. The latest jobs report on August 2nd sparked some global selling and has likely begun a trend higher, which the Fed has acknowledged.

We do not seek or welcome further cooling in labor market conditions.” Powell said, adding that the slowdown in the labor market was “unmistakable”.

A fun little fact emerged on August 21st from the BLS (Bureau of Labor Statistics), they misstated 880k jobs that were created over a 12-month period. Combine that with last year's revision of -359,000 jobs, and the BLS has overstated job creation in the monthly data over a two-year period by a stunning 1.117 million positions. The March 23’-March 24’ average of 240,000 was actually 174,000.

How are we to take these monthly numbers seriously, when they are constantly revised (higher and lower), and the BLS admits they were off by nearly a million jobs? The fact is markets trade off the report, accurate or not, but admissions like this make the whole thing feel like a charade.

And if labor is now the bogeyman, then what does a 100bps rate cut campaign in a four- month span signal what the Fed sees coming? Granted, the Fed’s economic forecasting skills match those of just about every other professional one, as they aren’t very good at it. Not at all really.

But with markets at near all-time highs, respectable economic growth, a strong labor market, and pesky inflation (sorry Fed, inflation is not “dead”), is it really time to initiate a cutting campaign? Make no mistake about it, they will cut rates as advertised. The genie is out of the bottle and the die is cast. But is it warranted?

And before we all rejoice and assume that lower rates automatically equate to higher asset prices, like its ever that easy, let’s look at some past statistics:

When the central bank started a rate cut cycle on January 3, 2001, the S&P 500 fell about 39% over the next 450 days, and unemployment rose 2.1%. When the Fed started a rate-cut cycle on September 18, 2007, the S&P 500 dropped 54% over the next 375 days, and unemployment jumped an additional 5.3%.

This certainly doesn’t mean history will repeat. In 2001 and 2007 the economy was in much worse shape than now, and we are in the camp that market dynamics and the plumbing amalgamated with it have changed drastically.

The Fed typically starts cutting rates when unemployment rises 10-20 basis points off a cycle low. This time it is 90 basis points off. So maybe the Fed feels behind now and the cuts are warranted?

Will a Fed aggressive rate cutting campaign sink the dollar and catapult the yen to dangerous levels? Or is that trade over with? Also, why are we cutting rates with stocks at highs, with elevated food and shelter prices? Do we really need to bail out CRE bag holders and regional banks who gorged at the trough of ZIRP?

And as of August, the Fed had only shaved off a paltry 7% off its balance sheet which implies the loose conditions still are very much rampant and have been a (artificial?) boon to asset prices.

Government spending has juiced the economy for years now and no one in Washington wants to be responsible for slowing that ride down. A complete reset is needed and warranted, but unfathomable for those seeking re-election or election.

Someday it will change and it’s not going to be pleasant. However, one could have penned that last sentence 10 years ago and it would have fallen on the same deaf years it will today. The catalyst for change is almost always an unknown quantity. We’ll know it when we feel it, until then party on as the saying goes.

Sticking with the macro, on July 31st the Bank of Japan raised rates 25bps, the first raise since 2008. This was one of the sparks that set off the short-lived global sell-off in August. Sadly, the BOJ quickly apologized for their “error” and were summoned to testify at parliament on August 23rd. Thankfully, during that testimony governor Ueda reiterated the BOJ’s path of raising rates if inflation and economic expectations remain consistent. Ueda also blamed the sell-off on US economic concerns.

We say sadly and thankfully because we need to rid ourselves of the participation ribbons mindset that has seeped into the markets. Central bankers should implement the policies they see fit and let the markets react, and price them accordingly. Volatility be damned.

The incessant fed jawboning and attempts to massage markets has softened market participants into a pain-free mindset, in our opinion. The various responses after the August mini-swoon were incredulous. Some were calling for an emergency 50-75bps cut, others implored the SEC to investigate why the VIX fear index spiked to 65 on August 5th?. All this on top of the BOJ apologizing for raising rates 25bps for the first time since 2008.

What sort of nonsense is this? Market participants sign up for fear, pain, and anxiety. It is the side effects associated with potentially lucrative outcomes. Have we really reached a place where any discomfort is met with tantrums and cries for assistance? Maybe years of ZIRP has created this every player gets a trophy environment, or maybe society’s change in attitude has permeated into the financial markets.

Whatever the case may be, we don’t view it as a positive on any level.

According to FactSet, for the second quarter, with 93% of companies having already reported, the S&P 500 is expected to sport earnings growth of 10.8% on revenue growth of 5.2%. That's down from 11.5% to 5.3% a week ago. So far, 78% of S&P 500 companies reporting have posted earnings beats while 59% have reported revenue beats.

For the full year, projections are for earnings growth of 10.2%, down from 10.9% last month on revenue growth of 5.1%.

The S&P 500 closed out the past month trading at 20.2 times forward-looking earnings, down from 20.7 times a week ago. This remains well above both the five-year average (19.4 times) and the 10-year average (17.9 times) for the index.

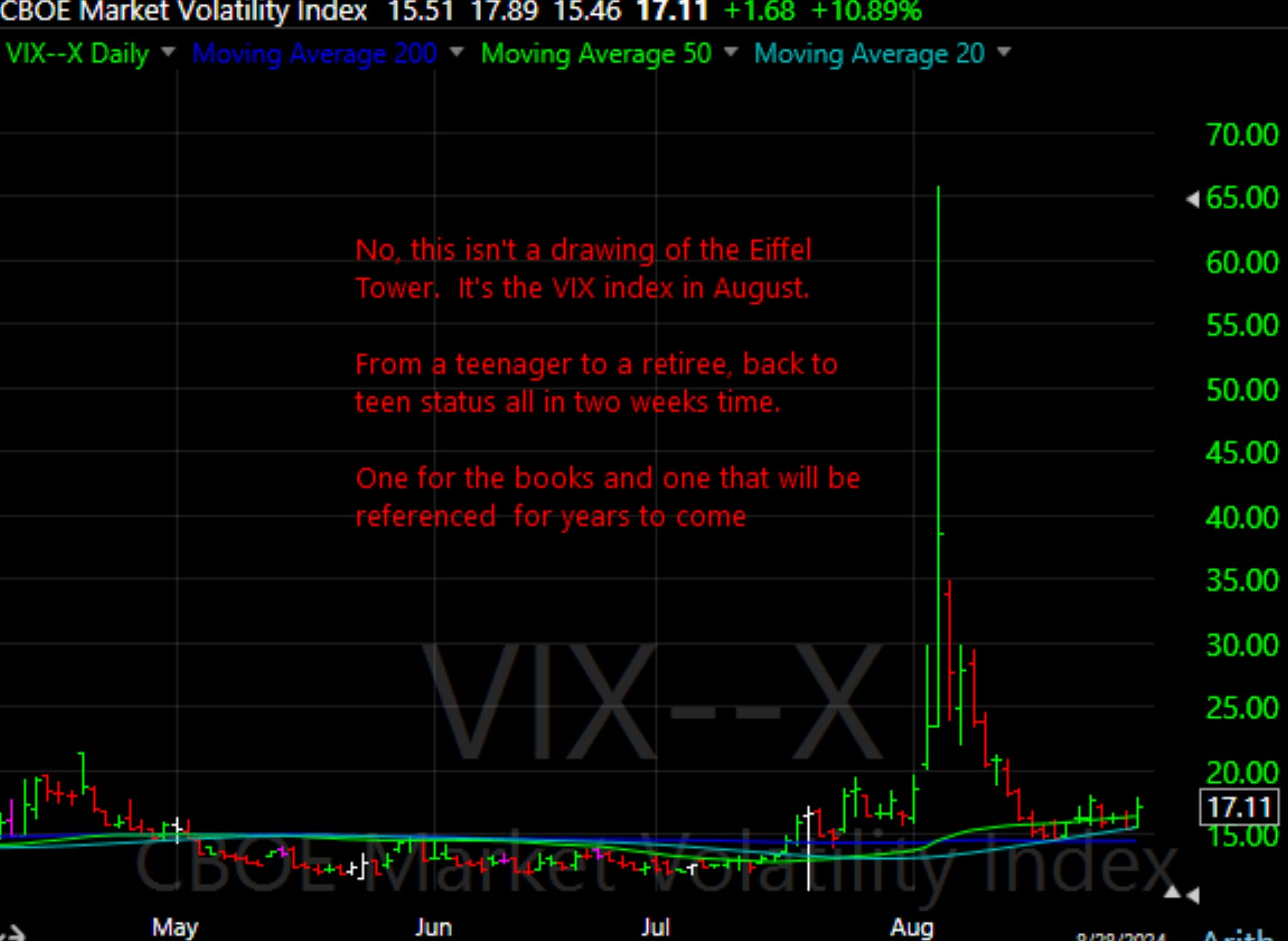

The overriding theme for August was volatility and when we refer to volatility we aren’t just talking downside. Last month was one of the more incredible short-term sequences for volatility (in VIX terms) in recent years, if not ever. Everyone assumes 2008 and the financial crisis would be the bellwether for a volatility explosion. And while it certainly was, it was more of a slow-motion crash rather than a violent event like we witnessed in August.

The VIX Index, or fear gauge, which had lulled us all to sleep for months as it withered away into a teenager, suddenly spiked to 65 on the morning of August 5th due to carry trade concerns and a Black Monday type event in the Japanese Nikkei. What may be even more stunning than the spike to 65 was the swift retracement back to almost 14 in under 2 weeks’ time. Truly one of the more dynamic moves the VIX has ever seen in its 31-year history.

If the fear of an unwinding yen/dollar carry trade and the massive potential for deleveraging across the globe that it could ignite was the spark; then what was the catalyst for the retracement? It’s unfathomable to accept a multi-trillion-dollar trade that has been in place for near a decade would be instantly unwound sans any major financial collateral damage occurring? Especially given that the yen stayed relatively strong against the dollar as the VIX was plummeting back to the teens.

“You can’t unwind the biggest carry trade the world has seen without breaking a few heads.” - Kit Juckes, currency strategist Societe Generale

We’ve highlighted in the past how financial markets have morphed into an online casino-like environment, fueled by easily accessible derivative products and leveraged ETFs/ETNs. This, along with increasingly elevated levels of computerized trading and algorithmic programs that continuously sweep the markets has constricted the time span for price discovery to days, if not minutes, as opposed to weeks and months as was the case years ago. The onset of 0DTE option trading is an increasingly huge factor as well.

Some other factors that contributed to the short-lived sell-off included ongoing Iran/Israel tensions, a tepid job report, Japan raising rates, and Warren Buffet dumping a sizeable stake in his Apple and Bank of America holdings. All these inputs seemed incredibly bearish over the first weekend in August, particularly when lopped on top of carry trade unwind concerns.

Bitcoin Update

Cryptocurrency is dead. Well, not officially, but it is asleep. The tedious range Bitcoin has been in for most of the summer, 55k-63k, has left the enthusiasts tired, frustrated, and searching for answers.

Fundamentally, the story has not changed. But there has been a rash of forced selling coming from the liquidation of Genesis, Mt. Gox, and from the German government. One would think most of that selling has been cleaned up already and already priced in, given that it was very public news. But weakness persists.

But all the positives, ETF inflows, Ethereum ETF approval, and slow adoption by state treasurers (Wisconsin), and institutions such as Goldman Sachs and Morgan Stanley, who became a top 5 holder of Bitcoin ETF IBIT this month in an attempt to satisfy demand from its large roster of wealth management clients that are expressing continued interest.

We are long-term crypto bulls, but it would be disingenuous to overlook the poor price action associated with perceived good news and not feel some discomfort. Particularly when you consider how weak the US dollar has been lately. Maybe the end of summer also signals the end of the malaise. The price action will tell us.

Space X was in the news this month as they were commissioned to attempt to rescue 5 astronauts from the space station. That, and the fact it will be one of the hottest IPOs in years when it does finally become public has led to speculation in some derivative space plays. Namely, AST Space Mobile, which soared 45% in August without a whole lot of news and has passed along attention to names such as Intuitive Machines and Planet Labs. This could be an area to keep your eye on if you are comfortable with speculation.

The fast/casual restaurant world continues to provide entertainment for traders. This month we witnessed Starbucks surge nearly 10% after Chipotle CEO Brian Niccole left the company for the coffee giant. Chipotle’s stock initially fell 8% but has recovered those losses. However, we must wonder now what the upside is for Chipotle going forward? They have lost their star CEO, their last earnings report was mediocre (stock dropped 2% in response), and Pershing Square, their biggest proponent, shed their stake by nearly 10 million shares in the most recent filing. And the brand seems tired.

Also, the competition keeps coming. Cava restaurants have been on a tear this year and just reported a 35% increase in revenues. Also, Sweetgreen’s continue to take share as evidenced by their 190% rise in price this year. Shake Shack is also back near its highs of the year while Chipotle remains almost 20% off its highs The fare at these establishments is obviously different than that of Chipotle, but the consumer dollar is fickle, and right now they appear ready to satiate themselves at venues other than Chipotle. At least that is what the stock prices are saying.

Commodity Update

Bloomberg ran an article this month highlighting the long bear market in iron ore, the key ingredient to manufacture steel, and how it has taken its toll on shares of steel giants Cleveland Cliffs, Rio Tinto, BHP Billiton, and of course US Steel.

But even at $100 per metric ton, it is still 700% higher than the brutal bear market prices from 1980 to the early 2000’s. Much of the blame for the malaise in steel is centered on China and their lackluster economy and overbuilt housing and infrastructure.

But what doesn’t consider is the $1.8 trillion of infrastructure spending slated for the next few years here in the US, and the Global Infrastructure Hub projects there will be $79 trillion spent on global infrastructure between now and 2040.

The non-precious metals finally got off the mat in August. Palladium and platinum both put in some potential bullish bottoming patterns and are in the process of trying to catch up to silver and gold. Gold set a new all-time high in August, to barely any fanfare or discussion. Which, if bullish, is exactly what you like to see. Silver and the miners are also playing catch up as well. However, silver has been awfully frustrating to trade in 2024.

Record projected yields in the grain markets have kept a tight lid on prices and kept short sellers, of which there are currently many, confident with their bearish bets. Canadian rail delays and occasional spotty weather patterns gave bulls some glimmers of hope, but they have been short-lived. The Pro Farmer Crop Tour came and went in August and confirmed that record, to near record, yields across the board are real possibilities. There has been some increased buying in soybeans from China, which was a sliver of light in an otherwise pretty dark summer for grain bulls.

Nvidia, the most important company on earth, ever, reported their Q3 results on August 28th, and they beat on every metric as assumed. Guidance was strong but given the negative reaction to share prices that followed, it wasn’t as strong as many had hoped. That is really the only small flaw you can point to in the release. Even more impressive is the $50 billion buyback announced, which is a mind-blowing sum.

Keep in mind that Nvidia currently represents 6.5% of the S&P 500 and 8.2% of the Nasdaq-100. Which is another mind-blowing metric. However, in the recent batch of 13F releases, there were more net sellers than buyers of the stock. And their biggest customer, Super Micro, was a target of a short selling firm Hindenburg this month and delayed their 10k filing to “complete its assessment of the design and operating effectiveness of its internals controls over financial reporting.”

The one question that gets louder every quarter is how will AI be monetized? Selling chips has been hugely profitable, as Nvidia has shown, but what is the next leg?

Moving on, the GLP-1 wars rage on and current undisputed champion Eli Lilly further distanced themselves from the competition this month when they announced Zepbound will be available via their self-pay channel for $399/month (2.5mg) and $549 month (5mg).

This, unfortunately, was a direct shot at both Hims and Hers and Viking Therapeutics, two companies we have been long in the past year. However, it should be noted that only 4.75% of the $315.6 million in Q2 revenues came from GLP-1. Nonetheless, the stock sank nearly 8% on the news and now has filled the gap from the May positive earnings news. Hopefully, after filling the gap at $14.67, it can find some support.

Remember when the bond bears were screaming “who is going to buy all our debt?” insisting that increased issuance would lead to a supply shock and higher rates? Well, turns out finding buyers is not a problem. Not at all really.

And it makes sense. One can earn a mediocre 3.85% on a 10-year yield here in the US. But peruse the globe and do some comparative shopping. Germany will give you 2.25%, China 2.2%, Japan a laughable .90%, and even our friends up north in Canada only offer you 3.1%. Only the UK has a slight edge at almost 4%.

If you want some reward, you need to take, you guessed it…risk. And risk right now means parking capital in Brazil (11.7%) or Turkey (15.5%) or Argentina (24.6%). That disqualifies a large swatch of interested parties, particularly those with risk aversion.

America has many warts, and they only swell with our ridiculous disregard for the $35 trillion growing national debt. But we are still #1 in the hearts of global fixed-income investors and will remain so despite what November may bring.

Looking forward and other Market Commentary

Summer has faded away and football season is up and running. Equity markets are entering their seasonally weakest period and with a rate cut looming on the 18th, it will be interesting to see if they are a panacea or an accelerant to the scheduled weakness?

The FOMC meets on the 18th as everyone knows and they will likely cut 25bps as everyone also knows. A 50bps cut would be a surprise (less than 27% chance) and likely lead to a large spike in volatility. But a 50bps hike doesn’t fit Powell’s methodology in our opinion.

The ECB meets on the 12th although not much is expected. The BOJ will meet on the 20th and that meeting will carry some extra weight as the yen strength continues to progress while more rate hikes are cautiously anticipated.

We have the CPI on the 11th, the PPI on the 12th, and the PCE on the 30th. However, barring a large change in the delta, these inflation readings are becoming less important now that rate cuts are here.

The biggest scheduled event of the month will be the August jobs report slated for September 6th. It seems comical to anticipate a report that surely will be revised, but market participants will, and we could see another bout of volatility like the one generated after the July report.

There are no earnings of real significance in September aside from Nike, Micron, Costco, and KB Homes. Earnings season will heat back up in mid-October.

We have two scheduled political debates in September. Which should be….interesting.

Finally, here in San Francisco the number of self-driving Waymo’s has increased exponentially in the past few months. Google has earmarked $5 billion toward the expansion of their fleet and regions, and it shows.

But a funny thing is occurring here in the city. People are using Waymo’s for way more than a ride to dinner. Dance parties, karaoke sessions, naps, zoom meetings, and “romance” are all now part of the Waymo experience for many San Franciscans.

It’s probably not what the programmers had in mind with their countless hours of test driving and algorithmic modifications. But it’s happening and it’s hilarious.

It’s refreshing to see people poke fun at big tech in the Bay Area, considering how dominant it is here. And just think you can have all that fun in a car and don’t feel guilty for not tipping the driver.