Round and Round

“I don’t know how to get this across to people. The US tripled its money supply in the past 18 years. It held interest rates at zero for nine of those years. Everyone thinks mortgage rates should be 3.5% and the stock market only goes up. Stocks were overvalued and interest rates were artificially low. How come no one thinks there is a price to be paid for that? All we are doing is returning to normal after a bender.”

-Brain Westbury, chief economist First Trust, X post 4/9

Well, where do we start? What a month, what a year, and what a time to be involved in the markets. "May you live in interesting times" is a well-worn cliché, but these days certainly justify dusting it off and placing it on the mantle.

It’s fair—and not political—to assess that the new administration's attempt to levy tariffs on over 180 countries, in the hope of seeking deals with all of them, has not gone as planned. And let’s be fair, it hasn’t been as successful as boasted. Liberation Day has come and gone, and the three key markets—equities, bonds, and the dollar—all saw volatile swings in April.

President Trump came in loud and confident, the opposite of Teddy Roosevelt’s “speak softly and carry a big stick,” and it has backfired thus far. Consumer confidence has eroded, and CEOs are frozen, trying to budget for a murky future regarding supply chain efficiency and tariffs. Stocks were on pace for their worst month since 1932 but staged a historic rally to finish the month flat. Bond yields have retreated somewhat, while the dollar remains weak.

The biggest complaint is the strikingly poor communication emanating from practically every tentacle of this administration. Not a day goes by without a social media post or comment from President Trump and his cabinet regarding trade talks.

China is in no rush to come to the bargaining table, as they stated on April 24th, and even Secretary Bessent said it could take “2 to 4 years” to get an agreement signed. We feel the administration failed to assess just how much clout they had with the Chinese and are now forced to play the waiting game as small businesses and supply chains suffer. Maybe a deal, or compromise, will be struck soon, and some sanity will return. Because no one will survive a 145% tariff for long.

Markets were buoyed in the latter part of April, lifted by repeated assurances of imminent trade deals. But these promises will lose credibility without signed agreements soon.

So far, in the early months of his tenure, the Trump administration has damaged the American brand. We have witnessed capital outflows in our equities, debt markets, and currency as proof. The most recent BofA manager survey showed that allocation to U.S. equities fell to a net 36% underweight, a 53% swing since February.

America is where capital is treated best, a principle we endorse. But so far in 2025, even staunch supporters of the President would take issue with that. Notably, Citadel CEO Ken Griffin, a prominent GOP supporter, had this to say on April 22nd:

“The U.S. is more than just a nation. It’s a brand…we’re eroding that brand right now…when you tarnish that brand, it can take a lifetime to repair the damage that has been done.”

Now for some positive feedback. The Trump administration, most notably Secretary Bessent, has shone a light on just how massive and unsustainable our debt is. Yes, their use of tariffs as a cure-all has been clumsy, but they are the first administration in years to admit that we have a problem, which is the first step.

DOGE was a step in that direction, although it was far less effective than advertised, and it has certainly created controversy surrounding the cuts that were made. Bessent knows we have trillions in debt this year to finance and wants rates lower, as does Trump, who threatened to “terminate” Chairman Powell this month for not cutting rates immediately—only to retract it days later, a prevalent theme in the first 100 days.

We are in the camp that a Fed rate cut(s) would do nothing to send the 10-year yield lower and could even send it higher, as we witnessed last fall. The case for cuts is just not there and should be shelved until an exogenous event (geo-political or credit) takes place.

In late 2024, Chairman Powell stated: “The U.S. federal budget is on an unsustainable path. The debt is not at an unsustainable level, but the path is unsustainable, and we know that we have to change that.”

Kudos to this administration for acknowledging and attempting to address problems we’ve long ignored and have papered over. But boos for their erratic delivery, poor communication, and tone, which are beneath both the offices they hold and the country they represent.

BITCOIN UPDATE

Decoupling was the buzzword in the crypto community in April. Did Bitcoin, and to a lesser extent Ethereum, finally decouple from equities and begin to trade independently, as gold and silver have in the past two months?

A larger sample size is needed to confirm, but at least the thesis is intact for now. After struggling to stay above $75k for a good portion of April, Bitcoin prices surged to over $90k in just two weeks' time. Many point to the ongoing capital flight out of the U.S. as a catalyst, combined with increasingly confusing messages from the administration, which have contributed to the flight into cryptocurrency.

The Bitcoin/gold ratio reached the upper 1.5 standard deviation band this month, while the current trendline is approximately 52oz of gold. This means that 50oz of gold translates to a $165,000 BTC price, while 100oz of gold would equate to $330,000.

Is this actionable and a reason to buy Bitcoin here? Not at all, but it’s fun to crunch the numbers and imagine where Bitcoin could go.

Much-maligned XRP rebounded from its early-month swoon and finished April up nearly 2% after the SEC approved 3 new ETFs. This is further proof of institutional adoption of cryptocurrency, while also strengthening the case for it as a legitimate asset class. It also helps bolster the argument for a small percentage allocation in all portfolios.

We are about to get a slew of earnings from crypto-related stocks, namely Coinbase (May 8th), Strategy (May 2nd), Riot Platforms (May 5th), and TeraWulf on May 9th. The miners will be of particular interest to see how they have weathered the lull in prices and interest in cryptocurrencies for a good portion of Q1.

Unfortunately, President Trump continues to harm the crypto community more than help it. This month, he announced a special meet-and-greet dinner for top holders of the TRUMP meme coin. TRUMP rose 19.3% in April after plummeting nearly 80% since its initial launch.

We remain confident that cryptocurrencies will thrive despite President Trump’s meme coin promotions and misleading claims about sovereign wealth fund adoption. The less the "crypto" President says or does, the better.

COMMODITY UPDATE

Energy prices bore the brunt of the selling in April, which aligns with the economic uncertainty we’ve highlighted, but is it justified? Oil traders were quick to price in a recession, while stock traders were quick to price in a temporary dislocation. Who is right? Crude has continued to languish around the $60 level after hitting a low of $56.70 on April 8th. April was the worst month for crude since 2021.

Even more brutal has been the decline of natural gas in April. After reaching 16-month highs on March 10th, natural gas has fallen 24% and is clinging above $3/btu. A sharp 7% bounce on the 28th followed blackouts in Portugal and Spain. We remain optimistic about the natural gas/data center power narrative.

With Memorial Day weeks away and grilling season approaching, we are being treated to record-high beef prices. Shrinking U.S. supply and uncertain future trade have caused live cattle and feeder prices to jump nearly 12% in 2025. Lean hog futures have surged 14.3% this year as well. Looks like it may be a Beyond Meat kind of summer.

Looking Forward and other Market Commentary

The main event for May will be the Fed meeting on the 7th. After all the threats and denials we've endured this month regarding the job status of Chairman Powell, the post-announcement press conference promises to be eventful. As for the Fed itself, it’s highly unlikely they will cut rates or alter their verbiage from the previous meeting. Not much has changed in that regard, and we are sure Chairman Powell will likely lean heavily on a “wait and see” approach to keep markets at bay for now.

Away from macro, while the bulk of earnings season has concluded, May still brings reports from notable companies, including Coinbase, Airbnb, Hims and Hers, Snowflake, Adobe, Palantir, AMD, Powell Industries, Oscar Health, and many others.

Major inflation data will hit on the 12th and 13th, and the PCE price index is scheduled for the 28th. However, barring an extreme shift in a government report, major market moves will likely be driven by government policy and tariff deal announcements—or the lack thereof.

Last month, Secretary Bessent claimed that foreign selling was not the catalyst for the bond market's mini revolt. Many remain skeptical of such claims, as the narrative makes sense from a political standpoint. This is why the auctions for the rest of the year will carry extra weight compared to years past. Currently, the U.S. will need $7-9 trillion to refinance maturing debt in 2025. Another $2 trillion will be needed to cover the deficit. A mighty task even in the most normal of times, much less in the current environment.

The Quarterly Refunding announcement relayed the following: From May to July, the Treasury will auction $125 billion worth of debt, including $58 billion of 3-year notes, $42 billion of 10-year notes, and $25 billion of 30-year bonds. Let’s all hope these auctions are well-bid.

The BOJ once again grabbed defeat from the jaws of victory as they punted away the chance to remain on a somewhat hawkish path and instead kept rates unchanged at 0.50% while revising down its near-term forecasts for GDP growth and inflation. They, not surprisingly, used tariffs as the reason. Japanese manufacturing readings, or their PMI, have fallen for 10 consecutive months now. The yen/USD cross fell nearly 2% on the news.

The April jobs report, which came out on the 2nd, was feared by many to show a sharp contraction in the labor force. It did not. The U.S. created 177k jobs in April versus the 133k expected, effectively quashing any hopes for near-term Fed rate cuts.

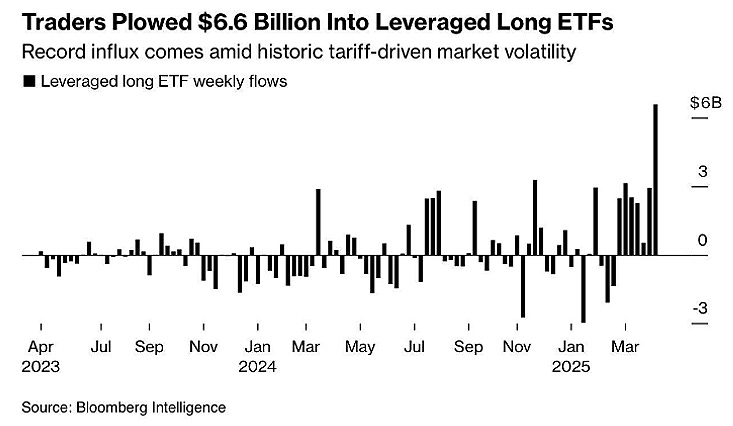

An interesting dynamic took place during the April stock swoon. The sellers were the "smart" money (institutions), as the "dumb" money (retail) was buying the dips. On April 3rd, the day after Liberation Day, retail investors bought $4.7 billion worth of stock, and since late February, have purchased nearly $33 billion worth of equities.

The gambling mentality remains pervasive, as we can see from the graph below. Leveraged ETFs and 0DTE options remained popular products despite, or maybe because of, the economic and market uncertainty surrounding ongoing trade dialogue.

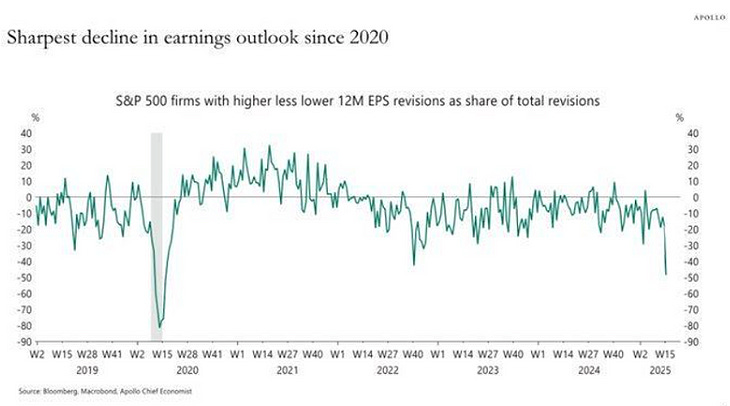

We are currently at the heart of earnings season, and thus far, results have largely exceeded expectations, particularly in tech. However, as anticipated, guidance remains cautious due to tariff-related uncertainty. We mentioned last month that any CFO worth their salt would use the current environment to avoid issuing any meaningful guidance, and that is precisely what we’re seeing.

As evidenced by the chart below, expectations for this year’s earnings are in freefall. We all know why, but the real question is whether the market is too pessimistic. Again, with the lack of guidance being given, it’s almost impossible to gauge. But we are in the camp that the pessimism is overdone, given the fact that market participants tend to “shoot now and ask later.” The same can be said for assessing earnings.

Meta once again was the leader of the pack in tech. Despite concerns about slowing ad spending, Meta posted revenue growth of 16.1% and earnings per share of $6.43, crushing expectations of $5.27. Operating income grew 27%, and free cash flow beat estimates by more than $1.7 billion. The stock rose nearly 5% in response. Microsoft also surprised the bears with a $0.24 EPS beat and raised their guidance for Azure growth.

Apple and Amazon both reported "fine" quarters and saw muted reactions with their share prices. Apple now gets 28% of its revenue from services, which is interesting considering it is always thought of as a hardware company. Amazon continues to grapple with increasing tariffs and was briefly targeted by the White House for admitting that tariffs were causing the rise in prices.

Overall, despite widespread pessimism, FactSet reports that the blended earnings growth for Q1 2025 is 10.1%, which would be the second consecutive quarter of double-digit growth.

Only 73% of the S&P 500 companies that have reported thus far have beaten EPS estimates, which is below the 77% average, but hardly a disaster. 64% beat revenue estimates, which is in line with the 10-year average.

The blended net profit margin is 12.4%, down from 12.6% in Q4 2024 but up from 11.8% year-over-year.

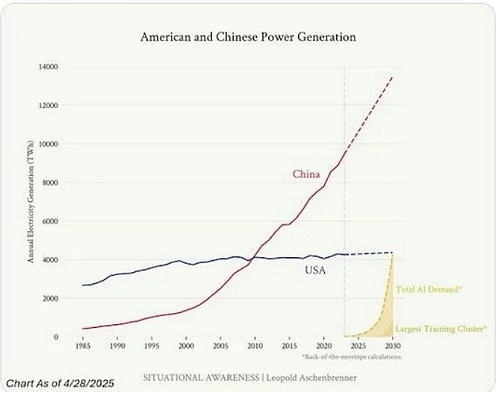

There was good news for the AI data center buildout camp this month. Meta raised its CapEx guidance from $60-$65 billion to $64-$72 billion. Microsoft noted that AI infrastructure demand is outpacing supply. And Equinix, a data center REIT, also raised its guidance, citing sustained AI-driven demand.

A recent research study out of Georgetown had this to say regarding the future of buildouts:

"Data centers to train and run AI may soon cost hundreds of billions of dollars and require power equivalent to a large city’s electricity grid if current trends hold. The co-authors compiled and analyzed a dataset of over 500 AI data center projects and found that, while the computational performance of data centers is more than doubling annually, so are the power requirements and capital expenditures.

By June 2030, the leading AI data center may have 2 million AI chips, cost $200 billion, and require 9 GW of power — roughly the output of nine nuclear reactors."

The graph below clearly demonstrates that we are losing the arms race to China in regard to energy production capacity. We hope this administration will prioritize this issue. Energy producers such as Constellation Energy and Powell Industries are well-positioned to benefit. We prefer focusing on energy providers over hyperscalers for two reasons: diversification (global energy will rise, AI or not) and more reasonable valuations.

Finally, there is a bill being drafted in Congress that would ban members of Congress and their spouses from trading or holding individual stocks. Named the "Pelosi Act" after Nancy Pelosi’s incredible trading acumen, boosted by insider trading information, which is legal in Congress as of now.

The fact that Congress can profit from insider trading is indefensible. Why are they given such a massive advantage over the constituents they represent? It’s nonsensical.

However, President Trump has his own meme coin, as does the First Lady, and Commerce Secretary Howard Lutnick, a vocal cryptocurrency advocate, has ties to Tether and MicroStrategy through Cantor Fitzgerald, which he headed until 2024. Eric Trump launched World Liberty Financial and American Bitcoin, raising over $500 million, with his family entitled to significant fees.

This month, Brandon Lutnick, Howard’s son, launched a crypto-focused SPAC, which soared 291% in April. We’d guess it would have been much more difficult to launch that venture without the Commerce Secretary as your father.

Nothing illegal has transpired, to be clear, but it does reek of a different sort of insider privilege.